I’ll do one better:

My payment card was just a bit too wide to fit in my cellphone’s cover. The phone’s own NFC antenna is at the top - and I use it all the time - so the card had to be at the bottom of the cover to avoid triggering the phone all the time, in portrait orientation so-to-speak.

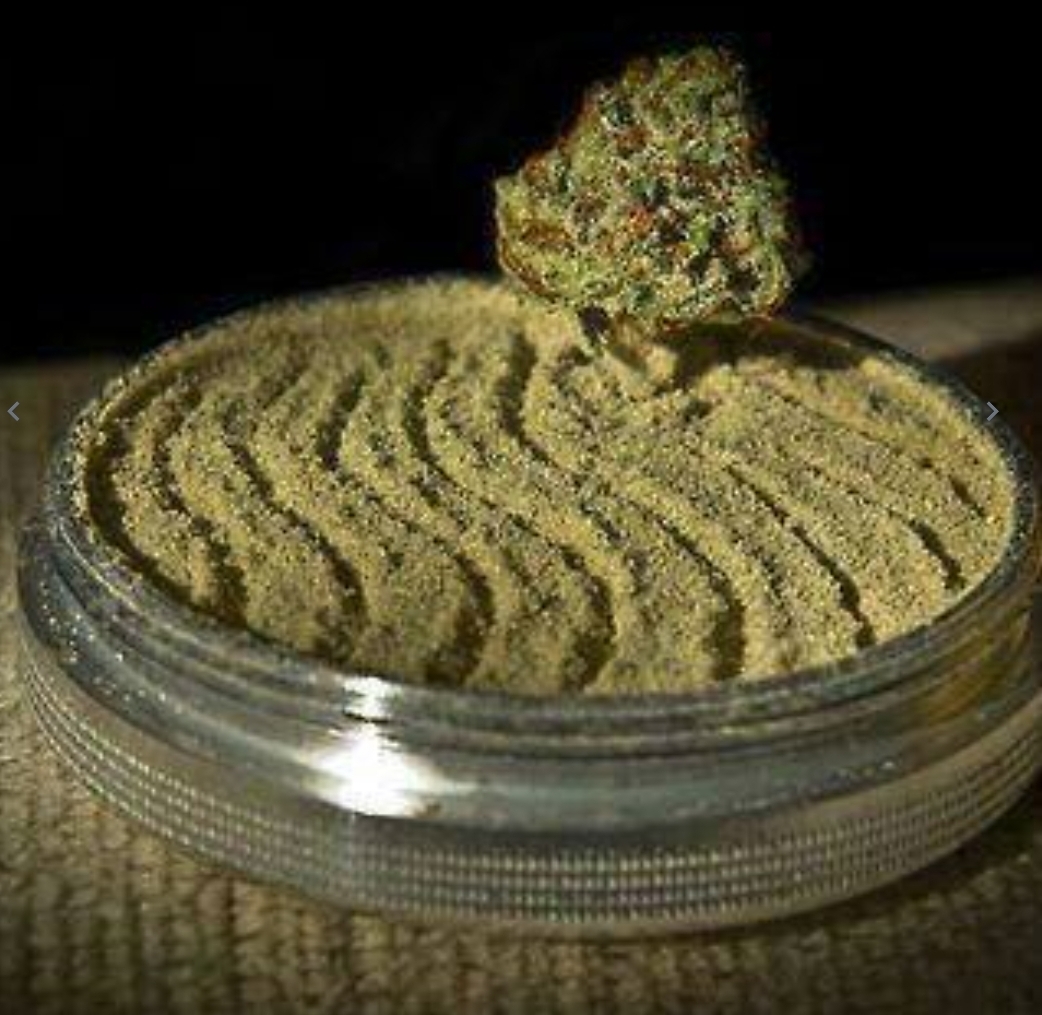

So I dissolved the card in acetone to extract the NFC chip and its antenna, then carefully reshaped one end of the antenna so it’s a bit less wide (and since I couldn’t modify the length of the wire or the number of turns in any way to avoid de-tuning the antenna too much, I sort of accordioned one side of the rectangle to accommodate the extra length of wire).

Then I set the new shape of the antenna permanently by carefully applying a piece of packing tape over it, flipped it over, taped over the other side to seal everything, then carefully cut around the new, ultra-thin, stubbier contactless payment “card”.

Now it fits really smartly in my cellphone cover!

Next time someone calls me a maniac, I’ll show them this.

Definitely doesn’t live up to their username.

The fact it’s secured with a piece of sellotape is just *chef’s kiss*.

You are fucking crazy. I love you.

>ExtremeDullard

>most interesting post???

Peak Lemmy behaviour I love it

I just wanted to say your dad is definitely proud of you dude

You just had to 1-up everyone here…

“Please use chip reader”…

I dissolved the card in acetone to extract the NFC chip and its antenna,

Wouldn’t the acetone also dissolve the insulation around the antenna wire? So when it touches itself, it shorts itself out, and – electrically speaking – you only have one turn of thicker wire?

Wire that thin is usually insulated with an enamel coating. I’d guess it’s either unaffected by acetone, or just tougher to breakdown. Allow the card to dissolve, but remove and dry asap, don’t let it linger longer than necessary.

Veritasium demoed this a few weeks ago while discussing tap-to-pay security and a vulnerability with apple pay+visa.

Only one way to find out, good thing that these don’t cost any money and you can just ask for a new one.

Maybe take some cash out first to cover any payments you may need to make it it breaks in some way.

If OP is using it and is happy with it, maybe one turn of wire is enough for it to still work, maybe with reduced range?

My guess is it wouldn’t work. On a magnetic antenna, the number of turns don’t affect range, but they do affect the frequency to which the antenna is tuned. It needs to be tuned roughly to the frequency the protocol operates on, otherwise it won’t work. In addition to that, these antennas also need to pick up power, which is also relative to the number of turns.

Seems like something to experiment with at some point. I do have access to test contactless card readers but not sure how they would feel about me destroying the test cards.

Well if it dissolved any insulation, it will not work, as the coil isnt even coiling. It is not a one big coil buy just two ends shorted(or as in the picture, a very small coil. Since this works i can only conclude coating does not dissolve in acetone

It depends on the insulation used, which can vary a lot for thin enameled wire.

Ty, great idea will try it

Have you ever run into difficulty with needing to authenticate with chip+PIN? Like while traveling?

That would be my big concern with this; it would make it very difficult to pass a PIN check, to say the least!

Super cool idea. I might just try it myself and see if I run into issues.

What I modified was in fact a contactless payment token. It had the form factor of a payment card, but it only does NFC.

I have another card for chip+pin.But I almost never use it where I live, because all limits were lifted on contactless payments a few years ago. If I try to pay something really expensive contactless, it will ask me for the pin - which is specific to the payment token.

Do you mind if I ask what bank issued those? Why? Does the chip+pin also tap or are they features on totally separate cards?

I’ve never heard of a separate tap to pay token (outside of perhaps transit passes or like, arcade cards), and never a card based tap transaction that asks for a pin.

Payment tokens are very common. Usually they’re sold as keychains, wristbands or rings, and they’re provisioned to work with the myriad of payment processors out there - which aren’t banks.

in my case, it’s a token from iCard. The way it works is, it’s connected to a regular bank account number with an IBAN number (supplied by iCard when you activate the token), and you transfer money to it that you can then spend with the contactless token. The nice thing is, if you lose it, you can’t lose anymore money than you put on it.

deleted by creator

Fairphone 6 has an add-on exactly for this.

I looked high and low for one where I could place my creditcard size tracker that isn’t also a flip cover, just a simple cover with a creditcard slot seems almost trivial.

I love this.

Amazing, I have never thought of that! I have always carried my card behind the phone, which is a bit too thick for my liking, but this is such a great idea, thanks for sharing!

Wow.

You clever, I like.

That is serious dedication.

Kudos for the effort. With that said, this would definitely raise some eyebrows if you have to return the card when getting a new one.

I’ve never had to do that… Just say you lost it.

Depends on how fussy the bank is, but yeah.

The bank just mails the new card to me. I still have old debit cards.

Knowing the reliability of our postal services, I would very much prefer to receive it in person. Of course there are security measures (activating it only when you get it and so on), but still.

Our bank will just print a new one on the spot for you if you go to their office. As long as you’re ok with your name and card number not being embossed. They have to order away the embossed ones – but you can still pick them up in person.

Well, what if you need an actual card for identification in the bank or something similar? Do you just show them the dissolved one?

Don’t know about OP but gov ID works for that purpose. I’m more worried about when they go to a store that doesn’t accept tap.

I was thinking about this, and there are two easy workarounds, I think:

- If possible, get a second active card in the same name. Ideally, a full-identical cloned card. Not sure if this would be allowed, but if not…

- Add another authorized user to your account and never give them the card, then just dissolve that card for tap payments.

But, in either case, I do think you might run into a different issue: automated fraud detection sometimes requires me to chip+PIN, even for transcribed below the tap limit. This has happened to me when traveling. I don’t think there would be any way around that, and if you then fail to authenticate with chip+PIN, it’s reasonable to think that the bank would lock your card for contactless payments until you successfully authenticate the card again with chip+PIN. (To be clear: this is only speculation; not sure if that would be an issue in practice.)

So, I suspect that whether this would work or not might depend on your institution (or maybe jurisdiction?)

The only time I’ve gone to my bank in the last 20 years was to get a new card, or to open a new account at a new bank.

What does this even mean?

Screen side with call buttons

You could put the rubber bands in between the phone and the case, so it’s not on top of the screen.

Ewww using a case.

Ah, now I see it. Thanks!

Would be easy enough to print a custom case for this

Delete Plasma Mobile, get SXMO, disable touchscreen then accept calls with side buttons, ez

Yeah just use glue, smh my head.

shaking my head my head

You seem to have been sniffing some to be smacking your head’s head.

I feel like it was a joke directed at people using ATM machines and staring at LCD displays

Yeah I clearly overestimated people’s familiarity with this particular meme.

Suddenly we need to explicitly write /s again

Yeah, I’m afraid I’ve no idea. I’ll search, but to be sure I’ve got the right one, a link would be appreciated.

Oh it’s not any meme image I’m thinking of, it’s just a text-meme.

Take that Android! This works even with the phone powered off! It works even without the phone at all!

Wait…

Or you can just keep your card in your wallet, like you have done for decades

The privileged have to invent their own problems.

The problem is that I don’t cary my wallet with me for pretty much a decade now.

Didn’t have to carry a phone for decades.

Now I don’t have to carry a wallet and multiple cards 🤷♂️

Gotta carry ID, what’s one more card?

I don’t need to carry my ID most of the time

That’s silly, you’re supposed to always carry it with you

Nope, no such law in France

I don’t carry my id and digital state ID s are out either way.

Ironic it’s a monobank card, it’s mobile only and you have to use a locked unrooted googled phone (or an iPhone) because big brother said so.

TLDR: some woman did a facial recognition log in method, the bank said that the photos are not stored and deleted instantly, but because there was a Slovenian flag (looked like russian in the photo)in the background, she got her bank account blocked and the CEO posted the verification image online

Edit: wrong link

makes you wonder what the CEOs of all those age verification companies are doing with all the photos

We know that the NSA and probably whoever dedicated enough can potentially access webcams remotely too, and millions of kids now have cameras in their room at all times through their phone or computer.

Hope that doesn’t get too popular, I don’t want to have to carry a second phone just to make payments when I can use a much smaller card instead.

In other news, cash is foldable.

Good luck folding £100 without having a pretty big bulge in your phone case.

I don’t have british pounds at hand so can’t test… Why are you putting valuable stuff next to more valuable stuff, anyway? Like to have everything stolen in one go?

How often are you finding people steal your phone?

None because I try to avoid bringing it in the first place. It’s my 2FA box.

Just get this phone - a bit thick, but very pocketable.

I opened an account with starling partly because they have a real webapp, but you have to fucking log in with your phone, which is half the reason I want a webapp: because fetching your phone when you’re already at your computer is just a ballache

deleted by creator

Nope, the point of this bank is that it’s mobile only. No offices, no webapp.

Nope. The website says “get app” like 4 times. There’s a webapp but it’s for business stats only (like if you own a cafe). They are just trying to “appeal to the younger generation”, and one part of that is the app that spams emojis everywhere. Another part of that is furry stickers (“qr cat”) believe it or not; in physical, Telegram and Viber because everything in this damn country is held together by Telegram and Viber.

Now how about contactless payments without visa or MasterCard.

It would have been nice if crypto didn’t turn into a network of pyramid schemes.

Like, I am sympathetic to the idea. I mined a Bitcoin a long time ago (and lost it in intervening years). But holy moly, did it erupt into a tire fire.

GNU+Linux is currently being used to kill civilians in several wars, but we don’t feel the need to point that out every time somebody says they use Arch btw.

Good tech can be used by bad people without everybody having to distance themselves from the tech itself.

That’s not to say that BTC is good tech, but it’s a decent proof of concept to free digital transactions from monopolists and tyrants.

Even without the greater fool scam, it’s basic physics that a some dedicated servers will be more efficient than having every computer in a distributed network process every transaction.

And authoritarianism can be more efficient than democracy. Doesn’t mean I want authoritarism though

It’s not democracy though.

Whatever the ideals of cypto are, however user friendly could be made, in reality, it’s just fundamentally too easy to be abused.

As-is, it’s one of those “it would work fine if everyone learned it in detail, and grifters would go away” ideas, and that’s not going to happen.

Democracy is fragile and exploitable too, but it has a track record of working across general populations for reasonable lengths of time.

What kind of abuse are you talking about? I doubt you’re talking about a 51% attack, which is incredibly hard. I’m guessing you are talking about social engineering, like where some scammer gets a poor soul to leak their bitcoin wallet or something like that.

In these cases, yes a centralized payment system can be useful, because the authority in charge can just reverse transactions that are deemed fraudulent or the result of a scam. But that same authority can do things like ban all payments to Steam for porn games (like the recent Visa Mastercard drama). That same authority can say “GrapheneOS and Pinephone users aren’t allowed to make NFC payments”.

In cases like these it would be nice for there to be an alternative to centralized systems, at least for those technologically literate enough to use these alternative systems.

Non American credit cards when

I’m European, I technically have a MC credit card which I’ll use on the rare occasions I need a credit card, but the vast majority of the time it’s debit card or direct transfers (what they’re now calling wero).

Unfortunately Visa and Mastercard also own the payment network for debit cards in many countries in Europe.

France has the national CB system, independent from American systems. https://en.wikipedia.org/wiki/CB_Bank_Card_Group

A lot of European countries have their own debit card networks. Germany has GiroCard, Italy has PagoBancomat and so on. The problem is that those are national systems that stop working once you cross a border. Most cards are therefore cobadged with Visa or MC as a fallback system.

What’s needed to get rid of the cobadging (at least within the EU) is some kind of translation layer to bring the existing European systems together.

I’m pretty sure the EUnis quietly working on such a thing

monobank

context?

See my other comment on this post

I don’t think they’re necessarily sharing the photos with glowies.

To be fair, it somehow got into hands of the owner of the bank, who is very closely tied to the government

We can go even further and create some sort of physical tokens that we can give to each other. These token would be secure, completely private, waterproof and even work offline. Maybe we could even put some pictures on them and make them vision-impaired accessible - the possibilities are endless!

People forget that cash is a technology - a pretty good one too.

Banks are closing ATMs left and right. It is getting increasingly harder to withdraw paper money and it sucks.

I haven’t noticed, but my grocery store recently limitted their cash back to $40, so you have to split your purchases into separate transactions until you have the cash you want.

completely private

Cash is more tracable then most think: Article is in German

It’s nothing compared to digital transfers. Sure you can trace via serial number but that’s mostly safe for us normal people. With digital transfer the privacy leaks can affect us normal people as the data can easily leak or be sold, stolen.

Maybe a solution similar to this could work: https://github.com/nfcgate/nfcgate/blob/v2/doc/mode/Relay.md

Have the card at home sitting on a reader connected to your homelab, add NFC module to PinePhone and simply relay the traffic over network.

this can be useful too! https://f-droid.org/packages/de.tu_darmstadt.seemoo.nfcgate

probably requires root though

At that point one should just https://dangerousthings.com/product/vivokey-thermo/ and get a free thermometer as well

Works without connection too🔥

Contactless payment works without connection. Now, the technical marvel is that it works even if the phone is dead.

Nice meme, but for us out there with at least a fully virtual card (some companies provide such benefits), we need a real MyAss-Pay alternative

I recently found Walt, but it’s a work in progress for now. The app is avalaible though

Some banks issue stickers for phones without NFC. It’s another physical card but contactless only and very thin (probably with an aluminum strip antenna).

I’ve got this papery stuff, and circley metal discs that works in most places. Unfortunately it does have pictures glorifying some family of depraved paedos on it , but not easy to avoid that.

Carrying an actual wallet all the time is pretty inconvenient, but honestly, I’ve been considering getting back into cash for 2 reasons: 1) If more people use cash, it’s harder to legislate it away altogether and 2) so small-time vendors don’t have to pay taxes. I don’t mean the local grocery store (the big chains get audited anyway), I mean the person with a stall selling homemade smoked sausages in front of a store, or the guy by the road who sells smoked fish from the nearby lake.

Also euro banknotes don’t have people on it to avoid the whole paedo glorification thing, so that’s cool

Yup.

And while the monarchist EU countries do stamp their monarchs on their coins, there’s more than enough decent and interestin people on other country’s variants.

Like Austria stamping Mozart and Bertha von Suttner (first female recipient of the Nobel Peace Price).

Or Croatia putting up Nikola Tesla, a Serb from Croatia, on some of their coins, likely to provoke Serbia. Or perhaps to symbolize unity between Croatians and Serbians but I frankly doubt that.

Or France recently creating coins with three important French women on the 10, 20 and 50 cent coins: Simone Veil, Josephine Baker, and Marie Curie.

Greece put up a couple people who were instrumental in Greek’s fight for independence and, more notably to Europe as a whole, the mythical Princess Europa riding on Zeus - the literal symbol of pan-Europeanism is on Greek’s 2€ coin.

And that’s just a sample, there’s even more. Largely (ignoring the monarchies) people who genuinely deserve to be looked up to - or at least respected - are on the coins that have a person on them.

If you live in a country with 19th century banking where people still pay each other by IOU on little pieces of paper, then sure. In modern countries a lot of places only take electronic payments.

In my country there are both places that only accept electronic payments and places that only accept paper IOUs. Go figure.

I don’t go to those places, don’t need their stuff.

Don’t need much stuff really.

Glad to live in 3rd world shithole.

I refuse to shop at a place that doesn’t do cash.

It’s ok, there are temples around the country that will vouchsafe your ability to pay

sounds better than an electronic payments only dystopia tbh

Man, this really makes me wish we had a more modern or powerful successor to the PinephonePro (that I could actually order from outside the EU)

Did you mean to post this comment 4 times?

No, I got an error a bunch of times and it didn’t seem to actually post

Nobody here mention security?

Like with passkeys (getting better though) and encrypted RCS messages, this is a proprietary standard that still sadly offers way more security.

It is token based afaik and the secret is never shared or even readable by an attacker. This card can be stolen with a single swipe, all that is protecting you is the banking system being overly cautious and expecting their systems to fail, so you need to enter a pin code on higher transactions or your card is simply locked.

Paying with VISA card online is insane from a security perspective, made slightly less bad by requiring authentication with a proprietary TAN app.

{kind=link}